CPA Advanced Leval Advanced Financial Management November 2019 Suggested solutions

Advanced Financial Management

Revision Kit

QUESTION 1a(i)

Q

(a) Distinguish between "insolvency" and "bankruptcy" as used in business restructuring. (2

marks)

A

Solution

(i) Distinction between "insolvency" and "bankruptcy" as used in business restructuring.

➫ Bankruptcy can help those who can no longer pay their debts start over by liquidating assets to pay off their debts or creating a repayment plan.

Bankruptcy laws also protect companies in financial difficulty

where as

➫ insolvency is a financial situation in which a person's or a company's debts exceed its assets.

➢ Insolvency is a pre- requisite for bankruptcy but not every person insolvent is bankrupt.

Q

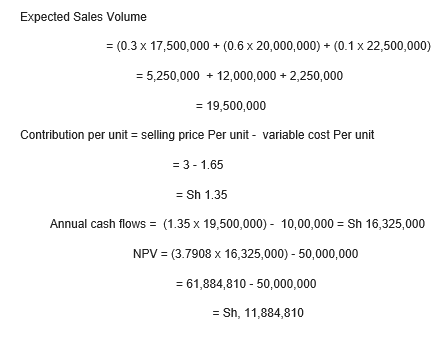

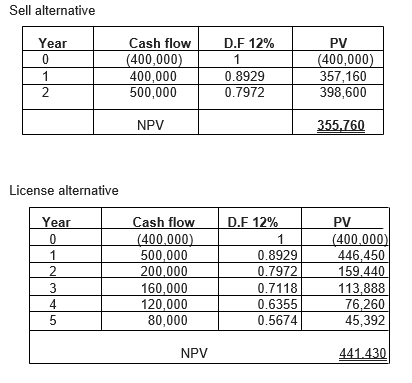

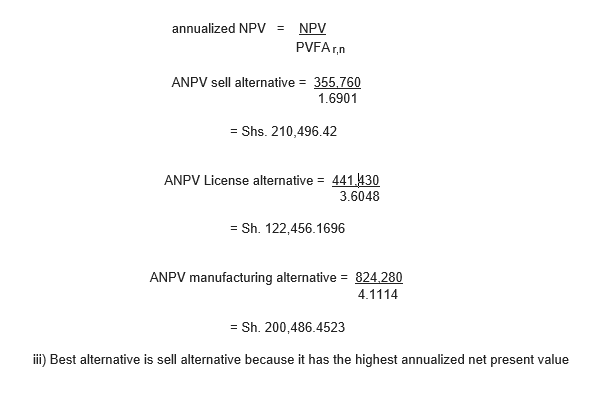

(ii) Advise to Kanga Limited on the best alternative based on Annualized net present

value (ANPV) approach.

(iii) Compare and contrast your results obtained in (a) (i) and (ii) above. (2 marks)

A

Solution

(ii) The best alternative

based on Annualized net present

value (ANPV) approach.

Q

(i) "Currency option" and ''currency swap' (2 marks)

(ii) "Interest rate swap" and "interest rate collar". (2 marks)

(iii) "Hedgers" and speculators". (2 marks)

A

Solution

(i) Difference between "currency option" and "Currency swap" .

➫ Currency swap consists of exchanging a certain amount of money in one currency for an

equivalent amount in another currency. By agreeing to a swap,two

companies are able to obtain low-cost loans and hedge against

volatility.

➫ Currency options are contracts that give the buyer the right, but not the obligation, to buy

or sell a currency at a specified exchange rate on or before a specified date.

Major difference of currency swap and currency option is that there is no exchanging of currencies.

(ii) Difference between "interest rate swap" and interest rate

collar".

➫ An interest rate swap is a forward contract in which one stream of future interest payments

is exchanged for another based on a specified principal amount.

➫ An interest rate collar is an investment strategy that uses derivatives to hedge an

investor's risk against interest rate fluctuations. An interest rate collar protects borrowers against

rising rates, while settling a floor that protects against falling rates.

(iii) Difference between hedgers and speculators.

➫ Speculators are investors who attempt to make a profit from a security price change while;

➫ Hedgers reduce amount of risk associated with a security's price change

Is one in which one company acquires another company in the same line of business. A horizontal

merger happens between firms who produce products that are

considered substitutes and compete with each other. The main benefit of horizontal merges is to reduce

competition

in the market in which the firms operate. These firms are also

likely to purchase the same or

substitute products in the input market.Horizontal mergers mostly lead to horizontal integration.

(ii) Vertical type of merger.

A vertical merger is a merger between companies operating at different stages of production or

producing complementary products, such as a leather shoe manufacturer acquiring a leather tanning

company. Vertical integration is considered backward when a company merges with a supplier and forward

when a company merges with a customer.

(iii) congeneric type of merger.

A Congeneric merger is a merger in which two companies are in the same industry or market, but do not

offer the same products in a congeneric merger. The two companies may share similar distribution

channels, which provides synergies to the merger.

A congeneric merger allows the target firm and its acquirer to exploit overlapping technologies

or production processes to expand its product line or increase its market share.

(iv) Conglomerate type of merger.

These mergers are neither vertical nor horizontal. In a conglomerate merger, a company acquires

another company in an unrelated industry, such as a telco company acquiring a printing company.

Q

(i) The maximum exchange ratio that A Ltd. should agree to assuming that it does not expect

dilution in its post acquisition earnings per share (EPS). (2 marks)

(ii) The total premium the shareholders of B Ltd. would agree to receive at the exchange ratio

in (b) (i) above.

(2 marks)

(iii) A Ltd. 's post acquisition earnings per share (EPS) assuming that the two companies agree

on an offer price of Sh.30.(2 marks)

(iv) A Ltd.'s post acquisition earnings per share (EPS) assuming that for every 100 ordinary

shares of B Ltd.. the shareholders are offered two, 12 % debentures of Sh.500 par value. (3

marks)

A

Solution

(i) Non diluting offer price = P/E Predator X EPS target.

60/4 X 3= Shs. 45.

Maximum exchange ratio = Non diluting offer price/Market price predator.

= 45 ÷ 60 = 0.75

(ii) New shares issued = Exchange ration x no of shares target.

= 3,000,000 × 0.75.

= 2,250,000 shares.

Total premium (Offer price target - MPS target) new shares issued.

= (45 - 30) x 2,250,000 shares = Sh. 33,750,000

(iii) Exchange ratio = Offer price/Mps predator .

30/60 = 0.5.

New shares issued = exchange ratio x shares target.

3,000,000 x 0.5 = 1,500,000. shares

Post acquisition EPS A = (Combined earnings)/(shares A + new shares issued).